Markets, Memes and MMT

MMT is winning the meme war, if not for the right reasons

TLDR:

The meme that government deficits don’t matter has become popular

For those who saw the ‘widowmaker’ (JGB) trade play out, that’s unsurprising

People can keep believing the right thing for the wrong reasons for a long time

Until employment and capacity recover, MMT memes are probably here to stay

Whatever MMT means to you and whatever your view on it, it’s clear that after years of being a hobbyhorse of nerdy irrelevant people like me it’s become a mainstream phenomenon. The publication of Stephanie Kelton’s book on “The Deficit Myth” marks a new high point for the popularity of its memes. I say memes not ideas because I am not in a position to say whether the ideas offered by MMT are correct, I am a fan of economics not an economist. From my vantage point as a market practitioner, my expertise and interest is in how the memes created by MMT affect the beliefs of other market practitioners and what that means for asset prices.

In general, ideas mean different things to us based on our experiences. I’m sorry if that sounds impossibly unscientific, but if you’re a market practitioner you’re in the second guessing business so you’d better have an idea of what’s driving others’ first guess. We all have limited brainpower and we apply it like the rest of our limited resources, wherever we think best. If some aspect of an idea is relevant to an experience we’ve had, we quite rationally seize on that aspect of it and seek to apply it in future because we cannot think of everything all of the time. We need the best thinking tools for our environment. If you consider the environment investors have faced for the past 10 years, it’s clear which facet of MMT has been the most relevant to them: Deficits don’t matter. More specifically, large government deficits do not mean disaster for a countries government bonds.

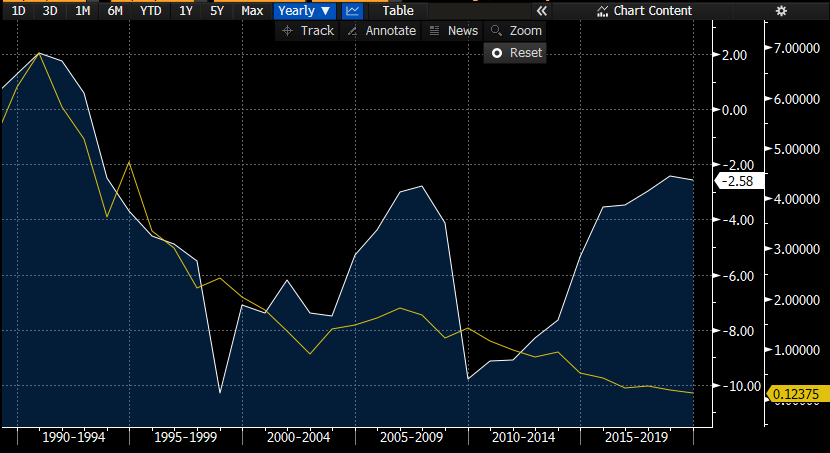

When I started in this business in 2011, choosing a government bond market to short was a matter of looking at projected government deficits and shorting the one that was biggest if you weren’t thinking too much, or the one that everyone else thought was the smallest but that you thought would be the biggest if you were a bit smarter. Naturally, if you thought in this way, you gravitated towards Japan. White here is the Japanese government deficit as a % of GDP, yellow is the 10y swap rate, sourced from Bloomberg:

Japan last ran a balanced budget in the early 90s and hasn’t looked back. In the aftermath of 2008, the budget deficit was as high as 10% of GDP, and government debt was already around 170% of GDP. In what came to be known as the widowmaker trade, none of this mattered - interest rates fell with almost no meaningful interruptions for a whole decade whilst the government continued to run deficits.

To those of us who’ve spent the last decade watching that yellow line grind down to zero, it’s easy to see how this facet of ‘MMT’ has caught on. Max Planck lamented that science advances one funeral at a time, but memes are on shakier ground than proper knowledge so they die easier. The meme that large government deficits lead to collapsing bond prices wasn’t based on any solid empirical or theoretical foundations, so it didn’t take much to kill. That’s not because there aren’t models out there that predict a relationship between large primary deficits and lower bond yields, it’s that those models weren’t being applied by market participants. They were applying the heuristic that big deficits cause bond routs. The same is true today of MMT and the “deficits don’t matter” meme.

In brief, here is what MMT says about government deficits. Governments face an inflation constraint, not a solvency constraint. So long as there are unemployed factors of production (labour, capital) it’s possible for government spending to employ those factors without causing inflation. With less than full employment, marginal government spending need not be accompanied by taxation. Therefore, government spending of newly created money at less than full employment is a responsible policy choice. That is a far cry from “deficits don’t matter”, but it’s also a really boring set of sentences, and most of them feel irrelevant to most people because we haven’t experienced full employment or inflation for the last decade. Why worry about those caveats when everyone knows we aren’t at full employment, and inflation, wasn’t that something we did in the 80s? Critics who attack the logical, theoretical or empirical implications of the MMT memes are missing the point - the idea that deficits don’t matter is popular because it agrees with experience.

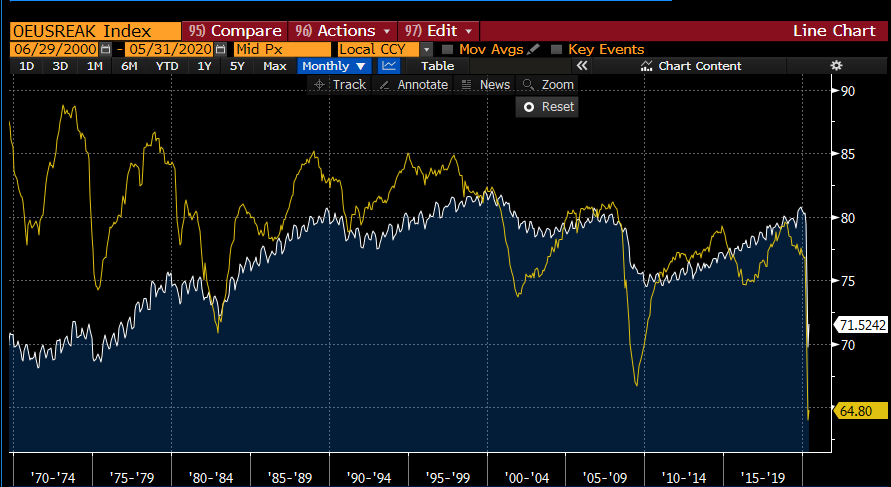

Critics of MMT assert that it offers nothing new. They’re right, in the same sense that Elvis offered up only reheated blues music. The ideas behind MMT are as old as economics itself, but that takes nothing away from the influence its memes are exerting in the present moment. The fact that people believe deficits don’t matter for the ‘wrong’ reasons doesn’t change the impact of their belief - which is to allow government bond yields to be on record lows, inflation expectations to be muted, and directly monetised government spending to be taking place almost everywhere. For now, the belief is likely appropriate. There is no sense in which the US economy is anywhere near any capacity constraint. The percentage of people aged 25-54 in the labour force has returned to levels not seen since the late 70s (white line). Reported utilisation of industrial capacity has never been this low(yellow line).

With 1 in 10 people who were in the Labour force at the start of 2020 now out of it, the idea that wages could rise meaningfully is fanciful to me. The idea that only 2/3 of the US’s industrial capacity is being used yet somehow prices might be able to rise materially seems implausible also. Indeed, employment rates took 10 years to make up the 5% dip in 2008, so even with double the pace of recovery from the present 10% hit we should expect another decade of spare capacity. The meme that deficits don’t matter seems destined to be with us for years.

NB: This post is not investment advice and is not a trade recommendation. The views expressed here are my own and do not reflect those of my employer.