Notes on the present crisis

Forgive me, for it has been some time since my last confession...

Hello again. It’s been some time since I’ve been moved to write but the last couple of weeks represent the start of a potentially historic shift in the global economic and financial regime and I want to get something on paper. Bear with me as I’ll be elaborating a lot of disparate thoughts and am more interested in comitting them to paper, getting some feedback, and refining as I go. There is a lot to say.

First and foremost, lets cover off the immediate actions. This is not investment advice. It is a personal account. For the past 6 months I have been gradually reducing my holdings of equity index etfs. Generally I am not a panicker, and I am not panicking now (indeed I probably don’t panic enough…), but on friday morning I:

- Sold just over half of my remaining stocks and equity ETFs

- Sold the very small amount of nominal fixed income I had lying around

- Sold about a third of my precious metals

- Allocated about half of the proceeds 50/50 between index linked gilts and ags

- Ordered about 6 months worth of the basic non perishable staples that I commonly use and can easily store in my loft

The only thing especially unique to me you should know is that I live in the UK, and have no realistic alternative to doing so, so index linked gilts are a logical choice for asset/liability management. And that I have a decent sized loft.

That’s really as far as I’d like you to read, but I’ll now get into the whys and wherefores, mainly for my own benefit.

Here’s what I understand of the present situation. After Trump reneged on nuclear agreements with Iran in his first presidency, they moved firmly in the direction of acquiring viable weaponary. At the start of the war, they had enough 60% enriched uranium to build a bunch of bombs eventually, and enough centrifuges to crack on towards weapons grade if they so choose. From a reasonably high base, they had materially increased their productive capacity for suicide drones, and cruise and ballistic missiles - moving both stockpiles and production to deep underground. They had reduced their electronic vulnerabilities by gutting and rebuilding their millitary IT infrastucture using Chinese technologies that have fewer or no vulnerabilities to US disruption. Political power was consolidated and dissent cracked down on. In short, they had become a more formidable regional power with the ability to asymetrically project force and survive external threats. Given Israel’s clear designs on regional domination, and the US’ unwillingness to tolerate a nuclear Islamic regime - Trump and Bibi’s impetousness seemed to make war an inevitability.

The war itself has proceeded along these lines. The US and Israel have pounded Iran, achieved almost total air superiority, greatly damaged its offensive capabilities and weapons stockpiles. Iran has retaliated by freezing shipping through the strait of hormuz, hitting a wide range of civilian and military targets to maximise shock value and keep its enemies guessing. The flow of hydrocarbons from the gulf producers has essentially stopped. Iran continues to demonstrate surprising offensive capabilities. Israel and the US appear to want nothing less than unconditional surrender - and there seems no realistic chance of this in the near future.

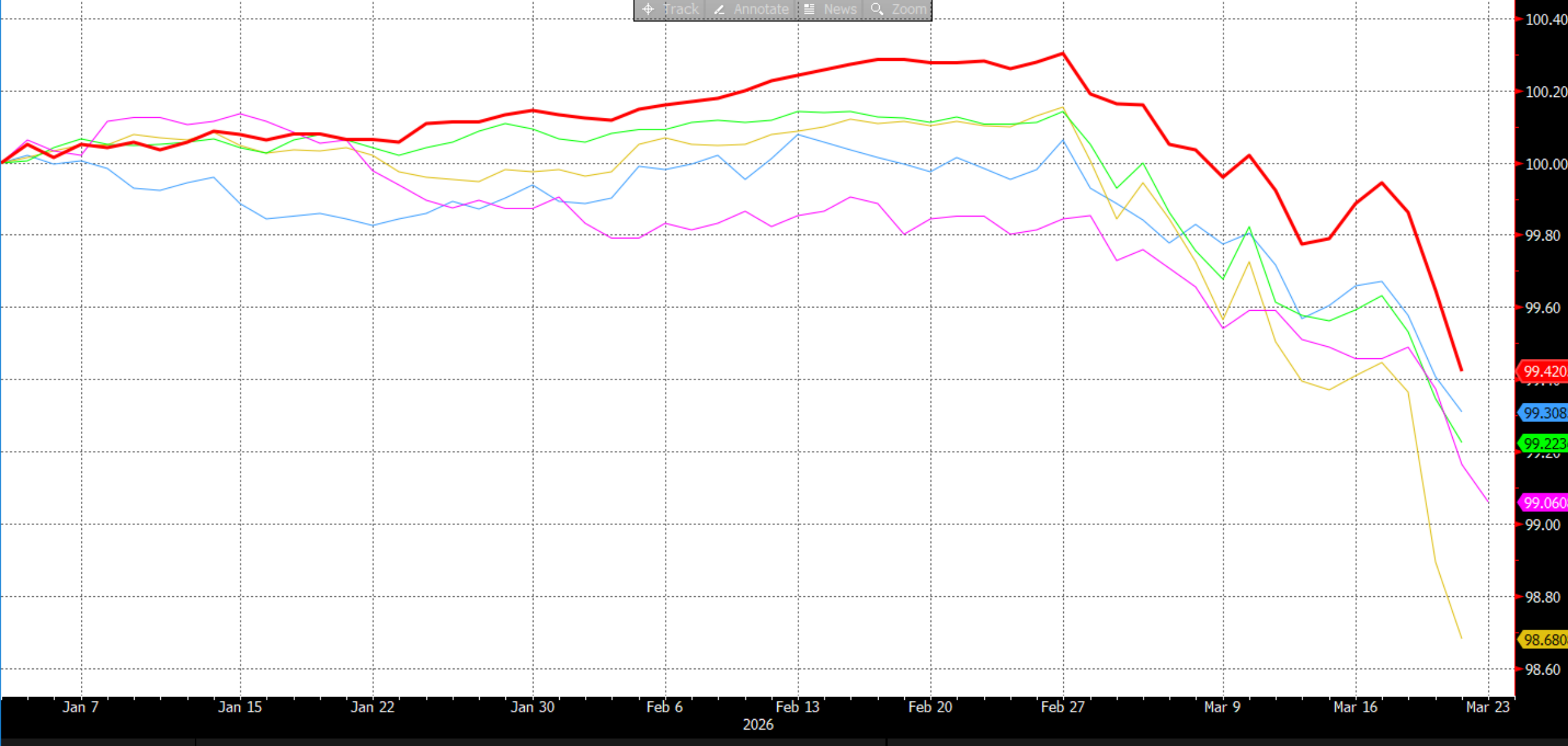

Here’s what I misunderstood. First, the extent of the markets pricing this risk. I’d noted rising Brent-WTI spreads (a good measure of the likelihood of non-US energy stress), rising inflation expectations, and the obviousness of the US military buildup. I assumed a reasonable amount of hedging and physical preparations had been done. How quaint. Second, the wildly skewed nature of market views on interest rates. My main analytical framework for generating trade ideas in rates means I’m normally paid of some things and received of others. I’d had a hard time persuading anyone to pay anything for the past 6 months but figured that was because I’m a bad salesman. My framework indicated the US was a modest pay, Europe, Sweden and the UK modest receives, Australia and Canada/Norway strong and modest pays respectively, etc. Applying the ‘i’m not special’ principle - I assumed most people were like that but with differences of opinion. My client base in the leveraged community turned out to be extremely received of every rates market under the sun. No judgement here, I am wrong enough often enough to have a good amount of sympathy. With all their advantages in information, analytics and risk management I’m sure they had good reasons. However I failed entirely to connect the dots of the flows I was seeing and conversations I was having. The last two weeks have been shocking as a market practitioner specialising in interest rate derivatives. If you are already nauseatingly famililar with this chart, apologies, if not well…

Dec26 settle short term interest rate futures in the first six countries I could think of. $ White, GBP Yellow, EUR green, AUD purple, CAD red. Rebased to 100 as of the start of the year.

Third, I didn’t understand the scope and extent of the secondary impacts of even a temporary loss of gulf hydrocarbons. So far the impact is yet to be acutely felt in the west - but in Asia it has been swift. Shortages abound. Many important production chains are simply shutting down. I had no idea how dependant world fertiliser production was on gulf exports. Or how little ship and airplane fuel was stockpiled and how that would inevitably impact supply chains.

These misconceptions were common. But I had little time to discuss them with clients this last fortnight. Mainly we’ve been arguing about whether this can resolve sooner than people expect, and whether all these central banks will really hike. The moves thus far have been peripheral stops and tail hedging - but the true stops have barely begun. We started to see them only late this week - both mentally and in the flows. With Baileys comments the sterling front end shanked to pricing multiple sequential hikes on Thursday and prices 84bp by year end as of Fridays close. On the same day, an initially quiet ECB was shattered by its own projections showing stress scenarios of 5% inflation and positive real GDP growth with unchanged rates, then a slew of hawkish ‘Sources’ headlines about immediate hikes. We now price 3 hikes for the year. $ was the last shoe to drop. The Fed merely talked the curve flat. But Fridays headlines on a possible US ground invasion leave us pricing half a hike by October. These moves occurred in such thin liquidity that the likelihood of any serious reduction in the very large received positions I believe are being held by leveraged investors is low. And it is only on Friday that people stopped asking me whether this couldn’t just all be over tomorrow and just got on with paying whatever they could stomach. For macro traders - the worst has now happened and we will be managing the consequences from here. This may seem like professional navel gazing, but it is relevant in considering the wider consequences.

For the wider world, in my framework, I don’t believe there’s any neccesary consequence to interest rate rises. Interest rates only matter on the stock not at the margin - by which I mean the fact that a bond yielded 3% yesterday and 5% today only makes a difference to the issuer when it issues more, and the investor who buys now. Similarly, you’ll no doubt fail to see any riches flooding in from the interest on your current or even savings accounts. However, the moves in rates markets form one of a few vectors that can cause the kind of balance sheet contraction that are one of the few reasons I am ever bearish nominal assets. There are likely others, but here are the ones I can think of roughly in the sequence I see them as playing out:

1. Leveraged investors are forced to liquidate. For many PMs the stops have already been painful. But the true stop for a leveraged fund is redemptions. Yes, gates will go up, investors are well locked in, but it doesn’t take much to start a cascade in the current conditon. It’s not only the big hedgies with good lockups that do leveraged trading. Banks, asset managers absolute return arms, corporate treasuries, the lure of high sharp low capital intensity returns is strong. It’s clear that there is a great deal of correlation between supposedly independent macro trading strategies. Exactly one of my clients went in net paid of UK rates. And he won’t mind me telling you he is not, position size wise, amongst the heavyweights. Clearly, intellectually it is another story.

I believe the losses on rates trading are already large enough to trigger a strong desire to redeem from leveraged trading strategies. I have limited expertise in quant/trend followers - but I don’t hear anything good there either. Relatively small redemptions after large NAV declines amongst a community who are outsized in their market compared to end user demand will I believe be enough to start a cascade of liquidations that have the potential to lead to ‘non economic’ moves in some key interest rate markets. By non economic, I mean normal arbitrage conditions break down. I started to see it on friday as the prices I was quoted by banks for various meeting date swaps (a popular instrument used by leveraged investors to express views on the short term path of central bank rates) started to move in opposite directions to the STIR futures to which they are collectively equivalent. It made for a challenging days broking, as I was obliged to explain many times to clients that whilst interest rate futures implied rates had fallen, the bid and offer for their particular desired meeting date swap had in fact gone up. This would persist for unusually long (10-20 minute) periods. That may not sound like a lot but the liquidity we are accustomed to in this space normally makes it quite impossible.

As the big hands unwind, my concern is that these dislocations persist for longer, or create truly perverse situations as both losing swap positions and ‘winning’ futures hedges are unwound simultaneously. Let us take as read the story I have heard that one leveraged fund is received of roughly $50mio a basis point of UK MPC swaps - losing average 25bp. Let us further assume that over the past couple of days they have hedged approximately 50% of that in futures, making 10bp on average. They now have some modest redemptions to meet as some investors have some rights and desire to cut gross leverage by 20%. What does that look like? At the same time as they are paying fixed in their swaps, and crystalising losses there, they must simultaneously buy back futures to be cash neutral to meet redemptions out of existing cash and be left with a viable business. How much are we talking?

- 50mio x 20% = paying 10mio/bp of swaps.

- avg loss of 25bp, -250mio cash.

- 50% x 50mio x 10 = 250mio available by buying back all 25mio/bp of their futures position.

Fridays volumes - on a day of extreme stress and much higher than normal volume - were worth 12.5mio/bp. Lets assume for laziness sake MPC swaps were half of that. So over some course of weeks one actor is paying 1 and a bit days volume of swaps, and buying 2 days volume worth of futures. Their swap dealer counterparties will naturally hedge by selling futures, which helps balance out their buying to an extent - but not entirely. The net is futures buying and swap paying at the same time. It is easy to see how dislocations could get quite substantial. Yes I am pulling these numbers out of my posterior at 11pm on Saturday night after drowning by sorrows yesterday - nothing but the best for my readers - but I mean only to illustrate a scenario. Lets heroically assume I got it all bang on. If futures correlation to swaps falls, implied volatility rises. That triggers more margin calls, more stops, etc etc. This might not be very good.

2. Secured financing of firms propagating to wider defaults. I’m on a roll making up numbers. In for a penny in for a pounding. 20% of global hydrocarbon supply is currently unable to reach the market. Lets say - and I believe this is very generous - 50% of that can be replaced by reserves, alternatives etc. That leaves 10% of global industrial supply chains unable to produce, well, anything. There is, I read, around 3.9trio per year of invoice factoring globally - most loans are 30-90 days - so lets say 650bio of outstanding. So 65bio, a drop in the bucket right? But… How do you as an investor know WHICH 10% of your invoices are now duds. The firstbrands blowup last year shows us they often do not even when problems are isolated to one company - rehypothecation and ambiguity over ultimate liability is rife. It’s easy to imagine an aggressive retrenchment of this type of credit. And given the crossovers between investors in factoring and the wider bogeyman of private credit - it is easy to see destabilisingly material reductions in lending. So facing an inability to finance receivables, plant etc, a 10% decline in activity and (using the OECDs 35trio estimate of global corporate bond outstanding and the ISHAREs ETF average maturity of 8.5 years), 1trio of refinancing needs per quarter on fixed redemption schedules…. Some pretty substantial defaults are possible. I appreciate I’m just conjecturing and laying out a well understand path here but it is worth thinking about in this context.

3. Wider collateral selling. Potential collateral sellers abound. EM Central banks are well enough reserved, but with import bills in many places about to skyrocket - those must be drawn down. With realised vol rising, clearing houses will demand more margin. Bonds and cash must be sought and posted, or positions liquidated (feeding back into step 1…). Gulf countries must finance defence expenditures, and increased living costs, whislt facing a collapse in export revenues. I hear they have quite a few treasuries to sell. They also invest heavily in supply chain and factoring… so feeding back into step 2. We are far enough into conjecture here that I’m happy not to bother with the scare tactic of making up numbers.

4. Monetary tightening. We are some weeks away from central banks raising rates, but raise them they will unless steps 1-3 play out so fast they become paralysed. As mentioned, the ECB project 5% inflation for 2027 and 1% real GDP growth in their ‘stress’ scenario with no rate changes. We are well into stress scenarios now. And that projection makes rate changes inevitable. 0% real GDP growth is ok, we live in a nominal world, but 5% inflation is not ok in any world for any CB. The monetary context matters a lot here too. In 2022 with the Ukraine war, 2 things were wildly different. Energy stresses were mostly frictional (russian gas didn’t stop for long), and we had just experienced a 100% + level shock to global money supply from the combined fiscal/monetary policy response plus a rate of change shock with a surprising expansion of bank credit. We are nowhere near that world now. Bank credit has been expanding a bit below NGDP almost everywhere of late, Australia, Canada and Norway being the exceptions not the rule. There has been no level shock - rebased to pre covid money and credit stocks are running below their annual ‘uses’ in most places. IB me for the charts. There is no slack here. Central banks tightening WILL impair credit. All of this feeds back into the other steps.

To put this in stark and memetic terms - this chain of self reinforcing financial processes combined with lower growth expectations is

In the wilder days of covid I was pretty pessimistic before the fiscal and monetary response kicked in - and wrote this. Applying some bond maths to equity markets you get a nice sense of how big % equity moves result from relatively small changes in corporate profits. A smarter man than me would be able to combine my monetary conditions monitoring with this in a proper way to tell you when stocks are a good buy or sell, but all I will do is wave at both frameworks and say ‘like that but the same way round this time’. The post covid policy response pretty quickly neutered the impact on corporate profits and provided vast monetary support for the market. This time we must expect almost nothing in this vein. Trump was facing an actual election in 2020. It’s not clear that he is now. His personal power and wealth are his main drivers along with vanity, and the former are disconnected from public equity markets. The feedback here will be through his vanity or by splitting his ruling coalition - not the ballot box or his net worth. I doubt he’ll act before things get truly unhinged. The UK’s and Japans bonds markets are on thin ice already. Europe has the fiscal taps half on and is probably the worlds best hope for a somewhat coherent policy response - and if that doesn’t underline my point I don’t know what does. I really do not think the bailout is coming this time from the fiscal or monetary side. And experience tells us you need both. Post GFC fiscal and monetary responses weren’t coordinated, and largely failed to ignite growth - it took 6 years to retake the 2007 highs in SPX.

Finally, and to round out this ostentatiously long piece - the opportunity cost of owning public equities has, I believe, fallen in real terms. The expansion of private ownership - fuelled by loose monetary and fiscal conditions as well as self reinforcing increases in elite power globally and a rise in political authoritarianism have meant much of the family silver has been sold to the rich uncle to pay the bills. Put simply, and I haven’t done the work here but I think it’s self evident, I don’t think the SPX represents anything like the market power it did. The stuff that insulates you in recessions - cashflows from utilities, affordable luxuries etc, the deeply predictable stuff you can leverage up on - has been asset stripped and the companies that used to house those assets are now deeply financialised. In the UK, a byzantine program of sell and lease back has led to the largest car park operator nationally going into administration. This was orchestrated, inter alia, by Macquarie who have been instrumental in leveraging up Thames Water - so if it’ll fit alongside the food in the attic I’ll be adding a water tank into the bargain. So theres all that. Plus the fact that the easy ride in terms of getting momentum factor returns via your index ETF are probably coming to an end as well. Whilst one potential silver lining of this is that the Spacex IPO ought to come to nought - the plan was for Nasdaq to change its listing rules to allow a lower free float - thereby forcing an enormous automatic purchase of its stock via index ‘rebalancing’. I have no doubt that this kind of nonsense is happening on a smaller scale already, and eating steadily into future returns.

So here we are. Its 12:30 on saturday night. The mind recoils. But this is how I see it. So we are publishing. Part of me still thinks I’ll wake up tomorrow to Trump, Bibi and the new Khomenei shaking hands, and a stream of red triangles in the centre of this map. That part of me has already cost me a good bit, and has probably cost my clients more via my indecision. The tuesday after it all kicked off I reccomended paying June ECB at 5bp priced. It made me reccomend cutting the trade at 11bp priced. I’m choosing to ignore it given its recent track record and clear emotional reasoning. Good luck to all!

*** NB - none of this should be construed as investment advice, all numbers, mentions of specific trades or anything pertaining to markets are a work of speculative fiction.

***** I do not use AI in my work except to read API documents for me and dump data into dataframes that I can then chart and look at as the good lord intended. I just write like this. Sorry.

How long do you believe the current deleveraging cycle will last?

Not sure I follow the cause of the decline (or reversal) of swaps futures correlation here. Can you ELI5?