The BoC tortoise and the RBA hare

Two superficially similar situations with a few crucial differences offer a classic macro trade

TLDR:

- BoC and RBA face similar economies, similar challenges

- CAD and AUD IRS are now almost the same curve, with a different starting point

- BoC faces higher money market rates despite the same overnight rate target

- BoC has much more debt it can buy, and more on the way

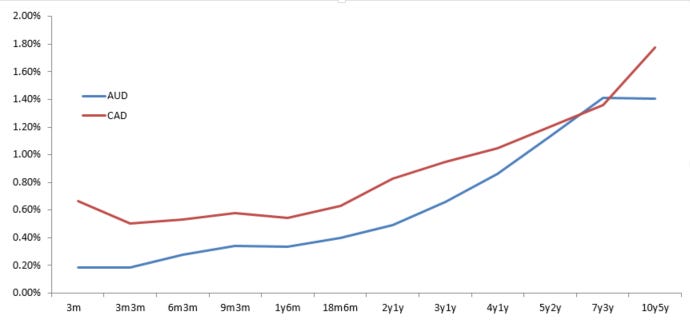

Australia and Canada have much in common economically speaking. Two rich, anglo, deeply financialised, current account deficit countries with relatively low federal debt to GDP and growing commodity exports in dirty industries. Their response to the Covid19 situation reflected the monetary space they both had. The BoC cut rates from 1.75 to 0.25. The RBA from 0.75 to 0.25. Both central banks increased their respective monetary base by about 25% of total M1, and moved to an excess reserves framework from a required reserves framework, meaning actual overnight lending rates are below their 0.25% targets. As one might expect, that leaves us with two similar looking forward curves. The below are derived from the spot interest rate swap curves sourced from Bloomberg (ADSW and CDSW tickers):

Almost identically shaped, though a little daylight between them at the very front end because the Canadian 3 month bank lending rate is some 0.4% above the BoC’s target for the overnight cash rate. This is the first difference between the two markets. The Australian money market is only loosely linked to the US, whereas Canada’s is tightly bound. Stress from the US libor/ois widening has crossed the border. In normal times, the 3m rate vs OIS is typically quite high - reflecting their unusual (for modern times) bankers acceptance system where banks guarantee the notes of 3rd parties. We’ll return to this difference shortly.

Now the second difference. The BoC had more space in interest rates, cutting from 1.75% rather than the RBA’s 0.75%. They have more space in another dimension also, that of assets they could plausibly buy. Both CB's have started QE in response to Covid19, but the BoC was slower off the mark, initially committing to buy 5bio/week of government bonds whereas the RBA managed to buy 36bio of bonds between the 19th of March and the 7th of April, before scaling back their purchases. The difficulty the RBA have is the relatively small pool of bonds they can buy - with around 600bio AUD of outstanding government paper. The BoC have around 800bio, but crucially almost the same size again of State bonds. Quebec and Ontario alone have around the same outstanding debts as all of Australian federal debt, and last week on Wednesday the BoC announced it would start buying them. Not only do they have this pile of debt to go after, but the Canadian Government are more determined than the Australian to add more. Instead of providing liquidity through the BoC, the government announced that it would buy pooled and insured mortgages directly. This is sure to mean more issuance of government paper.

In summary, we have one central bank facing high relative money market rates and a large and growing pile of debt to purchase, and another facing a small pool of assets to purchase with money market rates about as low as they can go. Two very similar economies facing similar challenges but with a very different monetary course ahead. The opportunity is there to get ahead of them. Hit me up on twitter, phone (+447708 462479) or email to follow through.

NB: This post is not investment advice and is not a trade recommendation. The views expressed here are my own and do not reflect those of my employer.