TLDR:

Everyone knows that everyone knows that inflation is coming

But not today, so they can stay believing that for a long time

And in any case, that belief is raising real rates, not expected inflation

Fade the narrative when the conversation moves to current inflation, when inflation expectations start rising and when inflation is misattributed to the ‘money supply’

After a large amount of form filling, agonising over travel rules and covid testing the BCLMacro family has returned to London - and just in the nick of time to enjoy a mandatory 10 day quarantine. The past few months have been a little eventful, hence the lack of posts, but things now look set fair and I look forward to sharing regular thoughts from my new base here in Kennington.

What’s clear coming back to the market and talking to people in it is that everyone knows that everyone knows that it’s all about the reflation narrative. Markets being the sum of guesses about others’ guesses, the truth of that statement is evidenced only by the fact that lots of people are saying it. Not only markets people but famous macroeconomists are weighing in to hand wring. Goldbugs, fake monetarists and mediamacro types are always on this particular trip so their unchanging gripes about the so called ‘fiat money system’ are well ignored, but the narratives peddled by economists and taken up by market participants matter for prices.

The way they matter is complex. A variety of different models illustrate the complexity of it, but the way I put it is that prices in the market are consistent with, and also form beliefs. I started to think this brief piece a few days ago and every time I sit back at the screens some interest rate somewhere is making a new high. At the same time, every bit of bank commentary I’m receiving mentions reflation on page 1 and clients are asking me ‘which steepeners are people doing?’, the presumption being that they must be doing something. We’re in a phase of the narrative where price increases are self fulfilling.

Of course, these things always come to a halt, and the mechanism for that is some data or event that shows the thing everyone knows that everyone knows could be wrong, and then IS wrong. The issue there is that higher inflation seems to be on the cards, and the reasons people believe it’s coming are coherent and sensible. My colleague Nivethan Tharmendiran recently shared a note on the cost and capacity pressures emerging in global transportation, some highlights of which:

Cargo Rollovers are a good barometer of shipping demand (and supply). They reflect how often ships are overbooked, risking exceeding the allowed tonnage, and cause significant disruption and delays (c.f being bumped off an overbooked flight and paid to stay in a hotel overnight). Not only do these rollovers cause costs to rise to shippers, but they also affect global supply chains given logistical disruptions. Rollover ratios are the percentage of cargo carried by each line globally that left a port on a different vessel than originally scheduled.

“Of the 20 global ports for which Ocean Insights collates data, 75% saw an increase in the levels of rollover cargo in December compared to the previous month.

Industry experts are now warning that the cargo surge could last well into 2021, with a strong likelihood that the prevailing conditions will continue throughout the first half of the year

Air freight cargo load factors are running at peak-season. Dynamic load factor methodology measures how full an aircraft is by considering both freight volume and weight. How full is the plane? ‘CLIVE’s ‘dynamic loadfactor’ analyses for the first four weeks of the year ending 31 January, based on the volume and weight perspectives of cargo flown and capacity available, shows a load factor of 66%, up 9% pts year-on-year. The global dynamic loadfactor for the last two weeks of January, however, saw an exceptional 10-15% pts rise over the same days of January 2020.’

His points have been reflected back to me in strategists notes and commentary, client chats, and then finally through the European data that came out last week. The slightly disappointing miss from US CPI last week however was shrugged off as a temporary blip. The problem with the narrative that frictional costs will increase inflation in the future is that it can’t easily be falsified in the present, which makes it hard to derail.

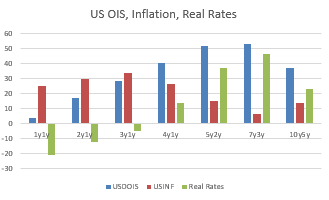

For now then we’re recommending trades that go with the trend, which interestingly is not for higher inflation expectations - but for higher real rates. Although most peoples perception seems to be that inflation expectations have risen a lot this year and this has driven increases in interest rates, but the reality is that inflation expectations have parallel shifted higher whereas interest rates have increased much more on a fwd basis. From Bloomberg, here are the changes in various forward swap rates from the 31Dec20, in basis points:

Real rates are substantially higher from 5y out in fwd space. It’s important to note that the ‘reflation’ narrative is mapping not to inflation expectations rising in the market, but real rates rising which indicates a more general optimism about future conditions. So not only is the narrative apparently impervious to being falsified, it’s not mapped to the price (inflation) that it’s ostensibly about. With two layers of insulation between the story and reality, it’s going to be tough to change for now. We’re looking at paying real rates via Gilts and Italian Linkers for the moment.

The question then is when and how the story changes. Whilst we’re talking about the possibility of future inflation and not relying on the market price of inflation to sustain the narrative that’s unlikely, so our first signpost on the road to retracement should be discussions of current inflation and the market price of it. So far, the famous 5y5y breakeven measure favoured by central bankers and market pundits has been absent from discussions, I look forward to its return. Then, I’d want to see an increase in market sensitivity to actual US cpi prints. The 4bp response we had to US CPI last week was an encouraging start. Finally, I’d want to see some misattribution of any inflation that does realise. Whilst realised inflation is being attributed to solid reasons of cost push inflation, as I wrote back in 2020 I expect that it will eventually be attributed to the rapid rise in monetary aggregates, central bank balance sheets and government spending. Indeed, discussions with clients indicate that these ideas are already getting popular. When they start to become dominant, that’ll be the time to fade the narrative, as the market will be ripe for disappointment and confusion.

NB: This post is not investment advice and is not a trade recommendation. The views expressed here are my own and do not reflect those of my employer.