The 70s that never were

What everyone knows about inflation, and why we think we know it

TLDR:

People think that loose monetary and fiscal policy generated inflation in the 70s and tight policy curbed it.

That’s far from obvious looking at history, and probably reflects ideological bias.

Now people think that inflation is coming because of loose monetary and fiscal policy, and that the Fed can curb it with rate rises.

Inflation will likely affirm the narrative in the short run and push rates higher.

As it does, the narrative and the higher rates supported by it become vulnerable to correction.

If an alternative view is right and monetary/fiscal policy can’t reflate the economy by itself, the narrative could collapse along with yields.

I’ve no doubt that there are many people who have a much more sophisticated and nuanced understanding of inflation than what I’m about to outline. I’m sure that you, dear reader, do. But what drives price action is not the beliefs of the most sophisticated but the views that everyone knows that everyone knows, just as it may not be the most beautiful face that wins the beauty contest. So here in brief is the common denominator view of inflation that prevails in financial markets.

"Inflation is the result of too much money chasing too few goods. Back in the 70s, inflation was rampant because governments spent too much money, central banks weren’t independent and helped them out, and labour unions made sure that wages and prices spiraled up together. Then, Paul Volcker asserted the independence of central banks and raised interest rates as high as they needed to go to cut money supply growth. Reagan and Thatcher broke the unions so they couldn’t keep demanding inflationary pay rises. There followed decades of central bank independence where inflation was kept under control. This time is different though. Many inflationary drivers are present. Huge government spending is coming for the first time in decades. MMT, an ideology of ever increasing money financed government spending, has taken hold at the Fed and US treasury. And now, the Fed has announced a determination to pursue full employment and tolerate inflation. Therefore inflation is coming. The Fed will react to it by raising interest rates. Whether I, the imagined representative market participant, am long or short bonds depends on my view of how the level of inflation, and fed reaction that is priced accords with my estimation of how far along this process is.”

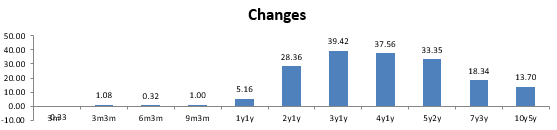

The view that I’ve described above playing out in response to the Feds communication is consistent with the price action we’ve seen since I sketched it out in my previous note. In those 3 weeks, we’ve seen 5y breakevens rise 20bps from 2.30 to 2.50, whilst the interest rate swap market has priced almost another two rate hikes into the curve. Here, the changes in various forward rates, in basis points between the 16th of Feb and today:

It’s also roughly consistent with the Feds communication and action. It is true that the 70s saw high inflation that disrupted economic activity, and that the Fed did nothing to curb it until Volcker. It’s also true that central banks have, since the abandonment of any pretense at exchange rate management in the 90s, told us that they raise interest rates to curb inflation and lower them to increase employment. And now they’ve fundamentally changed their communication, telling us that they won’t raise rates to curb inflation whilst they seek to raise employment to a maximum.

The problem with this story is how based it is in one experience. Since the episode of inflation and disinflation that brought about the modern era in central banking, inflation as measured by conventional metrics has been stable in the so called developed economies. Todays much talked about moves of 5y breakevens to 2.5% in response to what market participants say is unprecedented inflationary pressure from policy takes breakeven inflation only to the average CPI we’ve experienced since Volcker left the Fed in 1987. It may be true that this stability was the result of judicious management of interest rates by central bankers. But there are other possibilities.

To put it mildly, there was a lot going on macroeconomically speaking in the late 1970s. The relative stability of interest and exchange rates brought about by Bretton woods had proved too strict for a spendthrift US, and Nixon suspended gold convertibility and unwound the system of managed exchange rates that had prevailed since the 2nd world war in the early 70s. Freed from that constraint, there were two surges of broad money growth, one after the so called ‘Nixon Shock’ in the early 70s and one coincident with the ballooning of the Eurodollar market. Here for context the 50 year history of broad money growth (M3 YoY, White), inflation (CPI YoY, Green) and the Fed Funds rate (Yellow):

The first bump, as you can see above, comes after a substantial trough and so arguably was a kind of regression to the mean. The second bump was more of an event in its own right and coincided with a huge structural change to the US financial system. So far so consistent with the story we’re all familiar with of the inflationary 70s. Where the narrative starts to come unstuck is immediately after. Money growth had started falling before the Fed raised rates dramatically with the goal of curbing inflation in the early 80s, but actually started to rise once the Fed did so and continued to rise as inflation fell dramatically. It stayed high until the late 80s, and fell in the late 80s as inflation and interest rates fell with it.

Several features of this are at odds with the normal story. The idea that the Fed stood around doing nothing as inflation rose is at odds with what we observe - the Fed raised rates as inflation rose. At the same time, the surges in money growth that supposedly caused episodes of inflation don’t coincide, and precede inflationary episodes by years. Then, instead of rate hikes curbing money supply growth, they coincided with a renewed bout of it. The macroeconomic backdrop of the 70s squares this circle easily however. Two and a half decades of post war geopolitical hegemony for the US had given way to the quagmire of Vietnam and dependence on foreign oil, allowing oil producers to squeeze prices sharply higher. This on its own can account for the inflation shock seen in the late 70s (a good theoretical primer on how here). The persistence of the shock can be explained by tight and highly unionised labour markets that led to a wage-price spiral as unions attempted to recoup increasing living costs caused by the oil shock in wage increase.

There then followed a deflationary set of policies that had nothing to do with the fiscal and monetary stance. The US embraced Reaganite conservatism, unwinding large parts of the welfare state and destroying labour bargaining power which undercut wages. At the same time, capital flows were liberalised and industrial policy abandoned allowing production to be relocated to low wage countries. NAFTA and then the inclusion of China in the WTO ensured decades of low cost production. More generally, a free market ideology became dominant in policy making, which increased the bargaining power of capital over labour, reducing aggregate demand for any given income level (as the wealthy consume less, and wage demands were muted). These mechanisms are at odds with the prevailing ideology amongst market participants, the representative professional believes that wages are set competitively at marginal productivity and that trade is pareto improving.

Clearly it’s not possible to say definitely in the scope of this short piece whether that is sufficient explanation or whether the monetary and fiscal policies of the time played a starring role. Contemporary policy makers certainly thought they did. The point of this retelling of the story is simply to point out that people think they know, but they don’t really. Since then, we have had essentially no experience of inflation let alone successful monetary policy interventions to halt it. US CPI just about touched 5% in the chaos of 2008 before collapsing to outright deflation, but other than that has essentially rumbled along at low levels in the modern era. We have no empirical experience to draw on when we say that central banks can control inflation in a modern economy. Neither do we have experience of fiscal policy or any kind of policy generating inflation when its wanted, and plenty of experience of the opposite viz a viz Japan and Europe.

The reflation narrative then is vulnerable to a collision with reality. As I’m sure it’s possible to infer from the way I’ve written this piece, I am not at all sympathetic with the idea that monetary and fiscal loosening will increase prices. Here, capacity utilisation as monitored by the Fed (white) and the 25-54 year old employment (Yellow) rate of the US:

The modern era has seen a declining trend in capacity utilisation, troughing in this pandemic and not yet recovered to even the lows of the pre-pandemic / post GFC recovery period. Employment tells a similar story, declining since the peak of 2000 and only recovered to levels last seen in the 80s. With so many unemployed people and assets, I do not expect sustained inflation.

What I also expect though is that people do not look at it like this, and my view will be a minority one for some time. The next few months will see some optically high inflation prints thanks to the base effects of last years economic sudden stop, which sent practically every measurable economic statistic into a sharp decline in March . Price indexes were no exception. Proper economists will eye roll at the following chart, where i’ve drawn a rough trendline through the 2019/20 US CPI price index trend and extrapolated what YoY prints we should get in march and april this year if it holds:

If I do the same exercise on a 5y horizon, I can get a May print as high as 3.2%. That’s likely an upper bound as the 5y trend was steeper and we seem to have reverted more to the 2019/20 slope, but a responsibly constructed portfolio should probably be able to handle it. However it shakes out we are set for a quarter of robust inflation data with each monthly YoY print likely to be higher than the last. Call me cynical but I don’t believe that we are all sophisticated enough to shrug that off. Everyone knows that everyone knows that inflation is coming driven by central bank and government largesse. If the next 4 CPI prints from today (Feb’s is next tomorrow) go 1.4, 1.6, 2.4, 2.8 as my chart would imply, what will happen?

The inflation narrative I sketched out in my last post is currently focused on the inflation to come, the next few months will see it focus on the inflation already here. Investors think that they have learnt from the 70s and that loose monetary and fiscal policy means runaway inflation, and the prints they’ll get over the coming months will be consistent with that narrative regardless of what is actually generating the numbers. Base effects or no base effects, if this plays out, two things will happen in my view. Firstly, rates will push higher as we price both higher inflation and the Feds reaction. Secondly, the narrative will become precarious. As we move from a story about future inflation to current inflation, every print is an opportunity to falsify the story. Worse yet, if the narrative is based on such shaky ground historically it’s less likely to hold up to unexpected data. In my view investors will struggle to cope with a lack of evidence of re-employment of capital and labour as the ‘recovery’ progresses, so those data then become further opportunities for sharp pullbacks. I could easily be wrong about this and monetary /fiscal easing could have sudden effectiveness that we’ve not seen before, but its still true that there is a good chance that given their beliefs about the past investors will be disappointed.

The next few months of trading in FI markets then are about maintaining exposure to higher rates whilst the narrative is in place, whilst being clear about when to take profit as the reflation narrative peaks. As it does, the markets belief in a 70s that never was could offer an exceptional opportunity to be a contrarian.

NB: This post is not investment advice and is not a trade recommendation. The views expressed here are my own and do not reflect those of my employer.