The road to full employment

Looks short, but could be very long

TLDR:

The Fed is targeting inflation above 2% and maximum employment

Inflation will almost certainly exceed 2% for some time

Therefore, more focus on employment prints.

Data dependency normally means low conviction, mean reverting price action.

Regaining the pre-pandemic peak of employment could happen quickly.

Achieving true maximum employment would mean reversing decades of change.

For some months now I’ve focused on the reflation narrative as being key to price action. Those interested in buying bonds have been doing so because they find inflation expectations implausibly high. Those selling bonds have told me that they expect inflation expectations to head higher still. Both have in common that they are taking a position on where we are in the reflation story. However, the reaction to last weeks CPI number which beat expectations but was followed by a market rally in bonds, implies that we need to look beyond inflation to see which data will matter in the short term. From a few different standpoints, I think employment will be key.

First, there is the Feds publicly declared stance. Having moved explicitly to an average inflation targeting regime, they’ve also set the objective of labour markets reaching ‘maximum’ employment. When discussing policy tightening, first by reducing asset purchases, they’ve told the market that they need to see ‘substantial further progress’ toward this goal before considering taking any steps. The market has been very explicitly put on notice to monitor progress toward maximum employment. Second, there is a narrative emerging amongst market participants around labour market tightness threatening the recovery. The fact that business sentiment surveys are full of gripes about hiring difficulty at the same time the government is paying something approaching humane levels of unemployment benefit is highly triggering for certain people. The idea that the burden of macroeconomic adjustment should be born by involuntary unemployment amongst the most vulnerable in society is fairly popular amongst market participants, so it’s an anxious time for them as the Fed has been quite explicit that they don’t share this belief any more. Employment then is at the center of the Feds publicly declared reaction function, and a separate concern for those who try and second guess them.

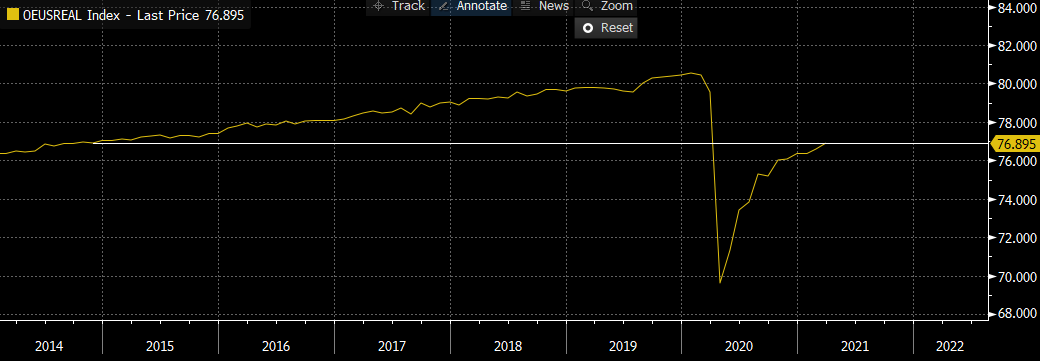

What then is the state of the labour market? If I had to choose only one number to illustrate the situation I’d pick the prime age employment rate, the proportion of 25-54 year olds that are currently working. The benefit of looking on a population level rather than at unemployment per se is that we don’t have to worry about flows in and out of the labour force. Unemployment can fall as people decide they no longer wish to look for work, but the employment rate won’t change . That’s a useful property in a pandemic where many have been unable to work even if willing. It’s also a useful property coming out as those who’ve been discouraged start to look for work again. Unemployment could not change at all whilst the economy strengthens as people are hired (unemployed => employed) and others start to look for work (inactive => unemployed). Unemployment could matter more if we’re interested in peoples behaviour and intentions, but we are interested in the economy as a whole. And here it is:

As the pandemic hit, the US had achieved a new high in employment. 80.5% of 25-54 year olds were working. As lockdowns hit, 10% of the population stopped working, but now only 4% less of the population is in work compared to the pre pandemic peak. That’s roughly where we were in 2014/15. That may not sound too bad but it wont be good enough for the Fed who’ve told us that they want to see maximum employment before they think about tightening. Not only that, but they want to see things get better for the less favoured in the job market, and as they’ve no way to counter misogyny and racism directly that means getting overall employment to new heights.

But which new heights? The issue with employment is that, at the risk of sounding a bit ivory tower, it’s socially constructed as well as an indicator of the state of the economy. The prime age rate data goes back only to the late 70s, but we have employment/population stats going further:

From the 1960s, women drove a trend of increasing employment as a percentage of the population, shown clearly by the comparison of womens employment rate (blue ) vs mens (red):

The pandemic saw the first time in post war history that less than 6 in 10 men were working. Much of this has of course to do with demographics, though not all - the prime age employment rate for men (green) has been declining also:

1 in 20 working age men were out of work in the 70s, now almost 3 in 20 are. The yellow line shows us that the trend boost from womens increasing employment stopped at the end of the 1980s, so lets assume that the Fed look at things similarly and consider the period since then the relevant one for comparison. Which maximum employment might they then target?

The all time high was in Apr 2000 at 82%. In over 2 decades, despite complaints of ever easier policy, central bank bubble blowing and all the rest of it, employment never recovered that peak. In fact we saw lower lows in each cycle. To re-achieve it then we’re talking about undoing decades of relative malaise.

However it may only be the last few decades of deflationary policy consensus that make that appear hard. The policy response to the pandemic has been unprecedented in scale and scope, and the pace of job gains so far this year, despite ongoing restrictions, has been rapid enough to put at least the pre pandemic peak in employment in view in the near future. Here I’ve extrapolated out the 25-54 employment rate using the last three months (red) and then just march vs feb (green). Market pricing for interest rates is shown in purple on the right axis:

Maintaining the past 3 months average gets us to the pre pandemic peak in employment in Q3 2022, maintaining March’s pace gets us there at the end of this year. Now, i’m not saying this will happen. It’s reasonably likely that the law of diminishing returns kicks in and makes each incremental gain in employment harder - the country re-opening being the easy part and re-cycling/re-purposing the productive capacity of the economy that’s been permanently shuttered by the pandemic being the hard part. For the purpose of forecasting movements in predicted interest rates that doesn’t necessarily matter however. There are as many views on the economy as there are economists, but there is only one view of the data, and everyone looking at the data can extrapolate it and make the same kinds of inference. Currently, the market prices interest rates only 0.2% higher than they are today (the Fed typically moves in 0.25% increments) at the time in the future that employment will reach the pre-pandemic peak if the last few months of job gains repeat. If the pace increases, as it did in March, we’ll reach pre-pandemic peak employment sooner - we’ll even be on pace to reach the all time highs of employment (82%) by the middle of 2022.

With at least a few months of CPI prints guaranteed to be well above 2%, and most likely above 3% YoY, it could be difficult for the market to avoid making this extrapolation. The average market participant at the moment believes that the Fed needs average inflation above 2% and substantial further progress towards its employment goals before giving a timetable for tapering, and we will have both inflation above 2% and a clear path to maximum employment if the numbers come strong.

However, I am no longer recommending outright shorts here. The fact that there is a data driven path to higher rates does not make for a compelling trading opportunity. With the Feds reaction function pegged to the employment data and everyone likely to therefore watch that data, the only edge one could have would be to correctly anticipate the data itself. I don’t believe I can do that. My contribution is normally in comparing the stories people tell about the economy to the reality and identifying where they diverge and then might converge, and if anything my read of that is pointing the other way. I’ve discussed the pre-pandemic peak in employment mostly when considering how market participants will extrapolate the next few months of employment data, but for true maximum employment there is much further to go. Even the 2000 82% peak in prime age employment came at a time when the labour force participation rate for 25-54 year old men was at 91%, 3% below its level in the 80s and 6% below where it was in the 50s:

It’s more than a bit of a stretch to imagine that the Fed is interested in remaking the economy in the image of the post war boom years, but it’s obviously true that a truly maximum employment targeting Fed has a lot more to do than simply allow expansion to the pre-pandemic level. Clearly they can’t mean that they’ll ensure that the last possible person who might be employed is before they raise rates but equally clearly the US economy has moved farther than people think down a path to lower employment. Given most people aren’t taking this into consideration, there is room for beliefs to shift toward the Fed being on hold for even longer than expected.

If this sounds like equivocation and failing to commit to a view either way, it is. Data dependency means that there is no unconditional forecast to make about rates movements. It’s true that strong employment prints can push beliefs in the direction of ‘substantial progress’ and rates can head higher. It’s also true that weak prints will push hikes further into the future. What I’m calling for here is an increasing focus on employment as the driver of price action in the near term. This should reward trades that take the other side of overbought or oversold price action and positioning. Beyond the next couple of months, the idea of maximum employment will have to meet the reality of a US economy that has been drifting away from full employment for decades. It’s possible that the Fed really will go for what they say they want, and seek to remake the economy radically, but given the political pressures that have taken us away from full employment it’s hardly my base case. We’ll need to wait through some labour market strength before finding out if the goalposts move.